STAKEHOLDER RELATIONS AND MATERIALITY ASSESSMENT

At Grupo Unicaja we have made a firm commitment to our stakeholders, whose vision and expectations are deemed essential in shaping our sustainability strategy and guiding the various lines of action we undertake. With this aim in mind, we work continuously to strengthen transparent, close and two-way engagement, thereby allowing us to integrate their needs into our decision-making and ensure our activity is aligned with their expectations.

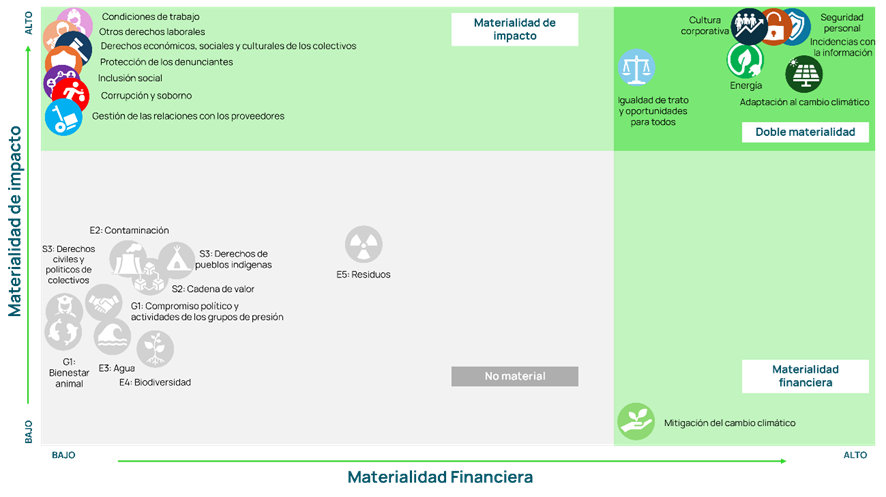

During the 2025 financial year, Unicaja carried out a review of the double materiality analysis previously conducted in 2024, using the same methodology, in order to confirm its validity and suitability for the context of the financial year, in accordance with the guidelines of Directive (EU) 2022/2464 (CSRD). This process forms a cornerstone of the 2025 Sustainability Report, available on the corporate website under the Sustainability – Sustainability Reports section, and enables the identification of the topics and subtopics on which the Bank must prioritise the management of its impacts and report relevant information.

Stakeholder identification and engagement

Unicaja recognises the following as its main stakeholders:

- Customers and users

- Shareholders and investors

- Employees

- Suppliers

- Regulators and supervisors

- Society in general

The identification of these stakeholders is reviewed on a regular basis, as are the communication channels enabled for each of them, including the corporate website, the ethics or whistleblowing channel, social media and other direct contact mechanisms set out in the Corporate Sustainability Policy. All of these comprise a permanent space for participation and active listening, helping to ensure their concerns are integrated into our corporate strategy.

A process aligned with the CSRD

In 2025, Unicaja carried out a review of its double materiality analysis, in line with the annual monitoring process established by the CSRD and the ESRS, with the aim of confirming the relevance and appropriateness of the material issues previously identified.

As part of this review, two main types of surveys have been considered:

- Surveys to assess the relative importance of environmental, social and governance topics, targeting the different stakeholders.

- Additional thematic surveys aimed at delving deeper into specific topics or using a different approach from that of the formal materiality process.

Based on the information obtained, Unicaja has reviewed and validated the impacts (impact materiality), as well as the risks and opportunities (financial materiality) affecting the Bank and its stakeholders. This process is based on a comprehensive overview of the Organisation’s activities and business relationships and involves the identification and assessment of IROs (impacts, risks and opportunities) linked to ESG aspects throughout the entire value chain, both upstream and downstream.

As a result of this review from a dual materiality perspective, the materiality matrix has been confirmed; it provides a visual representation of the issues deemed material in 2025, with no significant changes having been identified.

A management model aligned with European standards

The materiality analysis, which is due for review in 2025, forms the core of the 2025 Sustainability Report, providing a comprehensive overview of our ESG initiatives, commitments and progress. This approach allows us to confirm the relevance and validity of the material issues previously identified and reinforces our commitment to transparency, accountability and continuous improvement, in line with the requirements of the CSRD Directive and European sustainability reporting standards.

Regulatory update: Directive (EU) 2026/470 – "Omnibus Directive"

On 26 February 2026, Directive (EU) 2026/470, known as the Omnibus Directive, was published, introducing significant amendments to the CSRD with a view to simplifying and optimising certain technical aspects of the sustainability reporting framework.

Once this Directive has been transposed into Spanish law—by the deadline of March 2027—Unicaja will carry out a comprehensive reassessment of its double materiality analysis, in order to ensure full alignment with the new applicable European regulatory framework.

In doing so, the Group reaffirms its commitment to continuous improvement, transparency and the gradual integration of the most stringent European standards into its sustainable management model.